Private Letter Rulings - Car Donation Charity Loses Exemption

GiftLaw Note:

EO is a tax-exempt, nonprofit corporation under Sec. 501(c)(3). EO's purpose is to (1) provide financial assistance to middle and lower income families with hospitalized family members and (2) use the sales proceeds from car donations to fund charities of donors' choosing. EO consisted of two separate divisions, each with separate activities, websites and locations. CO operated EO's car donation program while Org operated EO's other charitable activities. IRS examination showed that CO was selling cars on behalf of donors, deducting a donation fee and then transferring the net sales proceeds to the donors. The donation fee was essentially an auction fee paid to CO for use of its lot and services. Examination of Org's activities showed that it had no documents substantiating any of its charitable activities.

Tax-exempt organizations under Sec. 501(c)(3) must be organized and operated exclusively for exempt purposes. Organizations that serve private interests or that do not operate for exempt purposes will lose their exemption. In addition, under Secs. 1.6001-1(e) and 1.6033-1(h)(2) organizations must keep appropriate records to substantiate their charitable activities. Here, the Service found that EO's separate divisions, CO and Org, were being operated in such a way as to warrant revocation of EO's exemption. First, CO was not operating for an exempt purpose because its car donation program was not engaged in charitable activities; it was instead facilitating car sales. Second, Org failed to provide any records substantiating its charitable activities. Therefore, the IRS revoked EO's exempt status.

Tax-exempt organizations under Sec. 501(c)(3) must be organized and operated exclusively for exempt purposes. Organizations that serve private interests or that do not operate for exempt purposes will lose their exemption. In addition, under Secs. 1.6001-1(e) and 1.6033-1(h)(2) organizations must keep appropriate records to substantiate their charitable activities. Here, the Service found that EO's separate divisions, CO and Org, were being operated in such a way as to warrant revocation of EO's exemption. First, CO was not operating for an exempt purpose because its car donation program was not engaged in charitable activities; it was instead facilitating car sales. Second, Org failed to provide any records substantiating its charitable activities. Therefore, the IRS revoked EO's exempt status.

8/26/2016 (6/1/2016)

Dear * * *:

* * *

ISSUE

Should the ORG's tax exempt status be revoked as an organization described under IRC 501(c)(3), effective July 1, 20XX because it did not operate exclusively for exempt purposes as described in section 501(c)(3)?

FACTS

Background Information

ORG was granted exemption as an organization described under Code § 501(c)(3) defined in Code § 509(a) and 170(b)(1)(A)(vi) in February 18 of 20XX. ORG (EO) was incorporated as a nonprofit corporation in the state of State on March 8, 20XX. Its State State entity number is: XXXXX.

The purpose of the organization as stated on its Form 990 as following: "To provide middle and lower income families with emotional and financial assistance while they care for hospitalized family members. To raise revenue from the Organization's car donation program and donate proceeds from the sales of the vehicles to a charity of the donor's choice."

ORG described itself on its website as following: "ORG * * *

ORG consisted of two completely separated divisions each with a different operational activities, websites and locations:

1.) CO Charity auto clearance located at Address, City, State Zip code (CO) Web address: www.website.com.

2.) ORG located at Address, City, State Zip code. (ORG)

Web address: http://www.website.org.

ORG filed Forms 990 Return of Organization Exempt From Income Tax for the last years as following.

Findings in examinations:

During the examination, the assigned agent sought information concerning the activities of the org and how it was operated during the taxable years at issue. The following narrative summarizes the information that was provided by EO concerning its activities and manner of operations.

ORG and CO are headed by a completely separated management and each has its own offices, bank accounts and operation activities.

CO is a used car dealership headed by Director, Director of accounting. It has about 20 employees and a few independent contractors (Car sales persons). CO signs contracts with other used car dealers (Donor) for bringing in vehicles as far as City to be auctioned at CO's lots. There were about 0 used car dealers in FY 20XX, only 0 remaining in 20XX. The contracts outlined and dictate how the proceeds are to be split between CO and the donors. The auction prices are set by the Donors. Basically, the vehicles were brought in already detailed (cleaned). When the vehicles were sold, CO deducts 0% buyer's fee, $0 smog check, $0 document fee and $0 donations. If the vehicle is not sold immediately, additional fees such as handling fee $0/week, Storage fees $0/day are added by CO. The remaining proceeds are returned to the Donors/other used car dealers.

CO used to conduct business with individuals who donated their personal vehicles. The donors would dictate in the auction contracts the desired auction prices, the portion of proceeds from the sales of the vehicles to be distributed to a charity organization of their choices. The portion of the proceeds would then be distributed to the designated charity organization upon the completion of the sales. However, this business has dried up in the last few years, affected by the recent law changes on tax deduction of the vehicles donated which limits the deduction of a motor vehicle to the gross proceeds from its sale. Individual donators do not have the same level of interest they used to have for donating their vehicles.

As the result, CO had turned its attention to conduct business with other used car dealers as stated above in the last a few years. There were very few donations made to charity organizations for the years under audit. The contracts between CO and other used car dealers do not contain a requirement to donate any portion of the proceeds from the sales of the vehicles to any charitable organization as it did with the individual donators. The $0 donations stated in the sales contracts between CO and other used car dealers were essentially an auction fee paid to CO for using its lot and services. Even the director of accounting of CO, Director, stated during an appointment that he did not think the $0 should be categorized as donations.

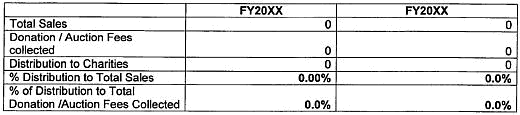

Total sales and the Donation/Auction fees for the years under examination are illustrated below. The amount of distributions was from a few individual donors.

The exempt program service from CO is virtually not existed in the year under examination. It is operation is no different from a regular use car dealership.

ORG Foundation Division:

As stated above, ORG is located in a separated address from CO. In Fact, it rents only a small office at the city of commerce City, State. It has no receptionist, staffs, or any assistants. CEO, CEO is the only person who runs this division. He can never be contacted directly at his office, or by his cell phone, one can only leave a message in the voice mail. It takes him a few days to return agent's calls if at all. POA and Director, director of CO has expressed the same frustration in contacting him as well. As CEO of the exempt organization, CEO does not appear to have any involvement in CO's operation. The two divisions appeared to run their operations totally independent from each other. The only one connection between the two divisions was that CO handles the payroll service for ORG and pays an annual salary of $0 to CEO. CO explained that this arrangement was to save money in payroll cost since ORG has only one person, -- CEO, CEO.

POA who is also the return preparer for EO that CO and ORG division each prepares its own G/L and send it to him for tax return preparation at the end of each fiscal year. CEO has always been late for sending in his G/L, and without any substantiation in the last a few years. POA has advised him many times in the past to correct such short fall and he has yet to make any changes. As a result, POA has stopped giving an independent audit opinion on its financial books for the past a few years. POA recognized the fact the organization has not had any meaningful charitable activities in the last a few years.

ORG reported gifting/distribution of $0 and $0 to the needy families in 20XX and 20XX respectively. However it has not been able to provide a copy of any approved applications or invoices associated with the gifts to the needy families. CEO had made a few promises to provide such records, but has never made good on his promises. The only records agent received from him was a copy of his personal cell phone bills which does not appeared to relate to any of the charitable activities. Other than the unsubstantiated distributions reported by ORG, it does not appear to have conducted any other charitable programs or services.

Both CO and ORG would have failed the public support test of 0.0% and the 0% facts-and circumstances test required by a 501(c)(3) charitable organization in the years ending on June 30, 20XX and June 30, 20XX.

LAW

Under Code § 501(c)(3), any organization which is organized and operated exclusively for educational purposes, of which no part of its net earnings inures to the benefit of any private shareholder or individual, is exempt from tax pursuant to § 501(a).

Code § 170(c)(4) defines deductible gifts as those that are used exclusively for religious, charitable, scientific, literary, or educational purposes, or for the prevention of cruelty to children or animals.

Regulations § 1.501(c)(3)-1(d)(1)(ii) states that an organization is not organized or operated for one or more of the purposes specified in subdivision (i) of this subparagraph unless it serves a public rather than private interest. Thus, to meet the requirement of this subdivision, it is necessary for an organization to establish that it is not organized or operated for the benefit of private interests such as designated individuals, the creator or his family, shareholders or the organization, or persons controlled, directly or indirectly, by such private interests.

Section 6001 of the Code provides that every person liable for any tax imposed by the Code, or for the collection thereof, shall keep adequate records as the Secretary of the Treasury or his delegate may from time to time prescribe.

Section 1.6001-1(e) of the regulations states that the books or records required by this section shall be kept at all times available for inspection by authorized internal revenue officers or employees, and shall be retained as long as the contents thereof may be material in the administration of any internal revenue law.

Section 1.6033-1(h)(2) of the regulations provides that every organization which has established its right to exemption from tax, whether or not it is required to file an annual return of information, shall submit such additional information as may be required by the district director for the purpose of enabling him to inquire further into its exempt status and to administer the provisions of subchapter F (section 501 and the following), chapter 1 of the Code and section 6033.

Rev. Rul. 59-95, 1959-1 C.B. 627, concerns an exempt organization that was requested to produce a financial statement and statement of its operations for a certain year. However, its records were so incomplete that the organization was unable to furnish such statements. The Service held that the failure or inability to file the required information return or otherwise to comply with the provisions of section 6033 of the Code and the regulations which implement it, may result in the termination of the exempt status of an organization previously held exempt, on the grounds that the organization has not established that it is observing the conditions required for the continuation of exempt status.

In accordance with the above cited provisions of the Code and regulations under sections 6001 and 6033, organizations recognized as exempt from federal income tax must meet certain reporting requirements. These requirements relate to the filing of a complete and accurate annual information (and other required federal tax forms) and the retention of records sufficient to determine whether such entity is operated for the purposes for which it was granted tax-exempt status and to determine its liability for any unrelated business income tax.

ORG POSITION

EO has not provided a position to this proposed action and, with this notification, will be provided the opportunity to respond.

GOVERNMENT'S POSITION AND CONCLUSIONS

It is the government's position that EO failed to operate exclusively for exempt purposes during the years under examination. In particular, EO is not operated for a charitable purpose under section 501(c)(3).

Given the EO's failure to conduct any substantial charitable activities, failure to the operational tests and failure to properly maintain records as required by the Internal Revenue Code during all of the years under examination, the exempt status of the ORG should be revoked and file U.S. Corporation Tax return effective as of July 1, 20XX.